The next decade offers tremendous opportunity in one of the world’s fastest-growing markets for digital infrastructure. As AdaniConneX breaks ground on one of the largest multi-billion dollar data center projects in the industry, João Marques Lima looks at how the company is gearing up in India and how the country’s hosting economy is changing.

Of the many data center markets around the globe, India is one of a kind. This proud, powerful nation is inviting a wave of greenfield investments in technology and communications but also holding fast to a green growth philosophy aimed at protecting the environment and precious natural resources.

India’s political leaders have spear-headed several initiatives to modernize the country, especially with ‘Digital India’, which has been called “the flagship programme of the Government of India with a vision to transform India into a digitally empowered society and knowledge economy.”

This has led to a ramped-up demand for data center capacity. Some examples of developments destined to drive such demand for the next phase of colocation growth in India include:

- Subsea cable deployments, internet exchanges and energy investments;

- New data protection laws, regulation and shifting policies;

- An increased shift from captive to colocation data centers with hyperscalers attracting enterprises;

- One of the largest “mobile-first” network deployments on Earth, preparing for 5G, and a big drop in data tariffs;

- The Internet of things (IoT) aligned with one of the world’s largest smart city rollouts – a US $28 billion project;

- Adoption of Edge computing to support the latter.

The need for more hosting horsepower is likely to grow rapidly in a nation of nearly 1.4 billion people, of which only around 52.5% (735 million) are online, according to the latest figures from the Telecom Regulatory Authority of India, released in December 2020.

To serve this rapidly expanding market, data center investors and operators are now even more focused on building out digital infrastructure to meet India’s growing needs and requirements, helping to realize the vision of a Digital India.

This is where things have gotten more interesting recently as one of the latest global brands to penetrate this market is global data center player EdgeConneX.

With an international portfolio spreading across North and South America and Europe, EdgeConneX currently manages over 50 data centers in more than 30 metros, from hyperlocal points of presence (PoPs) to hyperscale data center campuses worldwide.

In India, the Virginia-based operator has entered a joint venture (JV) with Adani Enterprises, the flagship company of the Adani Group, one of India’s largest multi-infrastructure organizations.

The JV will develop and operate data centers throughout India, leveraging the two partners’ complementary expertise and capabilities. To address the rapidly growing need for high-quality and reliable IT infrastructure, both organizations are committed to investing significant capital into the joint venture over the next decade to build out India’s leading green data center platform.

The project will run under the joint brand name of AdaniConneX, which will focus on building a network of hyperscale data centers in India, starting with the Chennai, Navi Mumbai, Noida, Vizag and Hyderabad markets. Development and construction at these sites have already begun with ribbon cutting events expected to take place in the coming months.

Commenting on his company’s latest achievement, Randy Brouckman, CEO of EdgeConneX, praises Adani as an ideal partner to expand in India.

“They [Adani] possess the necessary capabilities and unique expertise in India required to build out critical digital infrastructure that can best support our customers across the entire country,” he says.

Heading the Adani Group, chairman Gautam Adani praised EdgeConneX’s domain expertise and cutting-edge technology in the data center business, which together with Adani’s unique combination of green power, real estate expertise, access to undersea cable landing stations, and several nodes across India, will power the JV’s edge sites.

“We have been very impressed with the agility EdgeConneX brings to the joint venture,” Mr. Adani tells.

So, while EdgeConneX and Adani enter a one-of-a-kind industry JV, what is really driving the growth of the Indian data center market? And where is it happening?

Despite having a much larger population, the number of facilities in India is dwarfed when compared to other continents’ major population centers such as North America or Europe, both of which have less than half of India’s population but count with thousands of data center sites versus India’s fewer than 150.

Nevertheless, things are changing, and the country’s data center footprint is expected to accelerate in the coming decades, potentially climbing to the top of the global colocation rankings.

Let’s have a look at what’s happening and what analyst houses say about India’s present and future.

Let’s have a look at what’s happening and what analyst houses say about India’s present and future.

State of the Market

As of June 2020, India has 375 MW of data center capacity, according to a report from real estate and investment management firm JLL. As little as 27 MW were added in the first six months of 2020. However, a further 57 MW are preliminarily forecasted to have been delivered during the second half of the year, bringing total power capacity to around 432 MW. This is in line with other market reports, such as 451 Research’s “India: Leased Datacenter Market” which estimates the country to have 453.9 MW of capacity.

According to Anarock Capital Research & Industry Estimates, India has less than 1MW of data center capacity per million internet users. This compares to, for example, 8MW in the US and 21 MW in Europe.

Researchers, however, are not shy on their forward-looking projections and they forecast capacity to triple by 2025, reaching 1,076 MW and bringing India into the “exclusive“ 1 GW Club of nations. India’s additions of around 600 MW over the coming years amount to nearly the number China is expected to build in the same time period, figures from Arizton Advisory & Intelligence show. MW expansion also translates into a much-needed floor space addition, which JLL estimates to amount to 9.3 million sq ft in India to answer the country’s rapidly growing digital demand. Other market studies forecast up to 11 million sq. ft. to be built in the same time period.

Of course, capacity expansion means investment money, and capital expenditures supporting the growth of India’s data center infrastructure are estimated to reach US $4.9 billion by 2025.

Ramesh Nair, CEO and Country Head for India at JLL, says: “India’s data center market will outperform over the next five years, supported by a combination of growing digital economy, increased investor interest and stable long-term returns. Growth in the sector will be further powered by colocation sites which, via lower upfront costs, heightened data security, uninterrupted services and scalability will further influence investors to reimagine the potential of India’s data center space.”

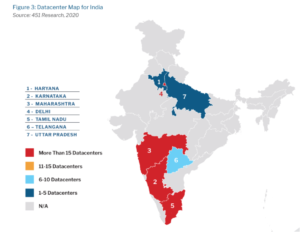

As for locations, India’s main data center hub is Mumbai, which amounts to about 42% of the market. The next two big destinations are Bengaluru and Delhi. Markets like Chennai, Hyderabad, Pune and Kolkata are also beginning to grow their data center footprints and are expected to become major hubs over the course of this decade.

Vacancy rates in India are low in real MW values. According to Cushman & Wakefield, Mumbai had in 2020 the lowest vacancy throughout Asia.

Chennai and Pune have the lowest vacant colo capacity at 6% and 7% respectively, closely followed by Mumbai with 12%. However, it is worth noticing that Mumbai – being the largest national market – accounts for more than 50 MW capacity, while Chennai and Pune, and indeed Kolkata (32% vacancy) and Hyderabad (32%), have less than 50 MW total capacity, with Delhi (41%) and Bengaluru (46%) just north of that.

As much as 43% of utilized colocation capacity is currently occupied by public cloud brands, about 62% of which host in Mumbai. JLL expects Chennai and Hyderabad to be the next frontiers for growth of cloud customers.

Supporting Infrastructure: Subsea, Internet Exchanges and Energy Investments

Today, India has 17 operational subsea cables, with Mumbai serving as a landing port for 10 of these. Four new cables are due to be turned on by 2023.

These include the SAEx2 cable linking Chennai directly to Singapore and Mauritius. Further development will eventually link into Cape Town and then on to Brazil and the US.

Elsewhere, the first of two Jio’s new cables is expected to come online next year. The India-Asia-Xpress (IAX) will connect Mumbai and Chennai to Singapore and interconnect with other far east countries towards the west coast of the US. The India-Europe-Xpress (IEX) will connect Mumbai to Europe and interconnect to the east coast of the US and it is expected to begin operations in 2023.

Lastly, and adding to the submarine superhighway that leads into Singapore, a fourth cable currently under construction – the IIP New Cable – will connect Mumbai-Chennai-Singapore.

Tata Communications with seven cables, Airtel with four, and Reliance Jio and Global Cloud Xchange both with three systems each, are the main players in India’s subsea infrastructure industry.

main players in India’s subsea infrastructure industry.

With subsea cables being laid, internet exchanges are also growing in India. The country currently counts seven exchanges offering IP Exchanges across India. This includes the AMR IX in Amaravati; Extreme IX in Mumbai, Chennai, Delhi and Hyderabad; Mumbai IX in Navi Mumbai; the National Internet Exchange of India (NIXI) in Mumbai, Chennai, Delhi, Kolkata, Bangalore, Hyderabad, Ahmedabad and Guwahati; and the AMS-IX India exchange, in Navi Mumbai.

On the energy front, 451’s analysts Dan Thompson and Jia Lyn Low point out that, in the past, India’s electricity supply was not exceptionally reliable, and it was not uncommon for electric power to cut off periodically. However, they write: “Since the Indian government’s Power for All program, that has been changing, and the electricity supply has been stabilizing. The country also has been investing in renewable energy production, with installed capacity contributing about a fifth to overall capacity.”

According to India’s Ministry of Power, the country’s full energy production amounted to 374 GW in 2020. Nearly 137 GW were produced using renewable sources, including hydro, biomass gasification, biomass power, urban and industrial waste power, solar and wind energy.

An advantage data center operators may have in India, is that they can directly negotiate with renewable energy providers, and they can also build their own solar or wind farms – very much like what is now taking place in the US and Europe.

This is one element of the joint venture EdgeConneX and Adani Group have entered into that is so interesting. Adani is one of the largest solar producers in India and AdaniConneX will be able to tap into those renewable energy sources to directly power its data centers, as well as leveraging Adani’s expertise in full-stack energy management.

The company, through its subsidiary Adani Green Energy, has, as recently as summer 2020, landed an 8GW solar power project worth $6 billion that will deliver the first 2GW in 2022.

Regulation and Policy

In 2018, several reports suggested that as much as 70% of India’s data resided outside the country – mostly in Asia’s data center hotspots of Singapore and Hong Kong. However, there is a rapid shift in data storage location as new legislation makes it compulsory to host Indian’s data within India’s national territory, a key driver to the India data center rush.

Additionally, state governments of Maharashtra, Gujarat, Telangana, Uttar Pradesh and Haryana are providing fiscal and other benefits for setting up data parks. Benefits range from providing subsidies on land, power, or other infrastructure, tax or duty waivers, grant of infrastructure/industry status, and classification as essential service.

Nevertheless, one of India’s biggest changes when it comes to set up a data center in the country – especially for foreign companies – is the Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation, and Resettlement Act that came into force in 2013. The act has been the cause of approval delays over the years.

“In some instances, this has led to delays in data centers being completed as the providers get stuck in a waiting game,” 451 Research’s Thompson and Low say. “In response, land banking is now a common practice – essentially acquiring land ahead of time such that all the permitting and preparatory processes are accomplished well in advance. While it does require some initial financial commitment, it helps to move things along when projects do begin in earnest.”

The Act has been put in place to protect landowner’s rights and provide “a humane, participative, informed and transparent process for land acquisition for industrialization, development of essential infrastructural facilities and urbanization with the least disturbance to the owners of the land and other affected families and provide just and fair compensation to the affected families whose land has been acquired or proposed to be acquired or are affected by such acquisition and make adequate provisions for such affected persons for their rehabilitation and resettlement and for ensuring that the cumulative outcome of compulsory acquisition should be that affected persons become partners in development leading to an improvement in their post-acquisition social and economic status and for matters connected therewith or incidental thereto.”

According to the National Association of Software and Service Companies (NASSCOM), India has “huge potential” to take a large share of global data center investments if it is able to act fast on implementing the country’s recently announced data center draft policy growing the CAGR by 2X-3X, with annual investments reaching $6 -$8 billion by 2025.

The Indian non-governmental trade association and advocacy group reports in its market study “India: The next Datacentre Hub” published in February 2021, that cumulative investments of ~$28 billion are expected over the 2019-2025 period, with the majority of investments focused on Tier IV facilities.

However, the group shares some key recommendations with government officials in order to entice the further development of the data center industry. These include faster implementation of the government’s draft policy, encouragement for the usage of renewable resources, a level playing ground for all players, faster regulatory approvals and digitization of requests for approval.

Debjani Ghosh, president of NASSCOM, says that increasing online focus – especially as a result of the Covid-19 pandemic – with the government’s call for being ‘Atma-Nirbhar’ or ‘self-reliant’ — and data protection through data localization all combine to make data centers a critical part of India’s data ecosystem.

She continues: “The criticality of data centers came to the fore during the pandemic when most businesses were unable to access their in-house servers during lockdowns, while data centers were still operating as they were deemed as essential services. Demand for data centers remains upbeat, despite the pandemic – highlighting the data center as the backbone of the ‘new normal online era’. Also, investments in data centers support growth opportunities for a number of allied sectors such as telecom, IT infrastructure and construction, further acting as a catalyst to boost the country’s overall economy.”

From Captive to Colocation: Hyperscalers, Enterprises and the Cloud Adoption Boom

The arrival of hyperscale players in India, combined with government and state policy initiatives to migrate to the cloud, has accelerated the shift to enterprise cloud adoption, according to Broadmedia Communications.

Large Cloud Service Providers such as AWS, Microsoft Cloud, Alibaba and Google Cloud all have a local cloud presence in India. Footprints by these operators are expected to continue to grow in the future, aligned with India’s internal growth as well as the country’s emerging role as a South Asian and global communications hub.

Enterprise spending on public cloud services in India is forecast to total $4.1 billion in 2021, an increase of 29.4% from 2020, according to the latest forecast from Gartner. The think tank says the fairly big jump in spend this year has been steered by the impact of the Covid-19 pandemic, a trend that is set to continue.

Sid Nag, research vice president at Gartner, explains: “Indian enterprises were not ready for the large-scale impacts of remote work. However, public cloud delivered on its promise of scalability, cost efficiency and business resilience for Indian enterprises during this critical time in 2020. As digitization efforts further evolve in the country, public cloud will become a must-have technology for Indian enterprises.”

India Public Cloud Services End-User Spending Forecast (Millions of U.S. Dollars)

| 2019 Spending | 2019 Growth (%) | 2020 Spending | 2020 Growth (%) | 2021 Spending | 2021 Growth (%) | |

| Cloud Business Process Services (BPaaS) | 186 | 5.8 | 184 | -1.1 | 195 | 6 |

| Cloud Application Infrastructure Services (PaaS) | 549 | 54.3 | 718 | 30.7 | 968 | 34.8 |

| Cloud Application Services (SaaS) | 1,133 | 22.7 | 1,156 | 2.1 | 1,365 | 18.1 |

| Cloud Management and Security Services | 251 | 22.9 | 276 | 10 | 362 | 31.2 |

| Cloud System Infrastructure Services (IaaS) | 696 | 60.8 | 816 | 17.2 | 1,180 | 44.6 |

| Desktop as a Service (DaaS) | 30 | 105.8 | 49 | 63.7 | 70 | 43.5 |

| Total Market | 2,845 | 35.1 | 3,199 | 12.4 | 4,140 | 29.4 |

Source: Gartner (November 2020)

Indian enterprises moved critical business applications such as email, web hosting, customer relationship management (CRM), enterprise resource planning (ERP) and human resources (HR) to the cloud, ensuring employees can access them anytime and from anywhere in the world, as long as they have internet access.

“While end-user spending on cloud in India is increasing, there is a long road ahead for Indian enterprises to achieve the same market maturity as the US or Europe. India-based organizations and their CIOs need to focus on the cultural shift that will make them cloud-ready and give them a competitive edge,” adds Nag.

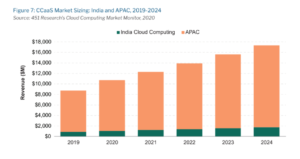

According to 451 Research’s Market Monitor predictions, the cloud computing-as-a-service (CCaaS) market in India will maintain solid growth with a compound annual growth rate (CAGR) of 15% up to 2024. With cloud being a technology foundation for the deployment of multiple digital offerings and services, revenue for CCaaS in India is estimated to exceed the $1.2 billion mark by 2024, with a CAGR of 16.3% throughout 2019-2024.

4G/5G rollouts

India is preparing to rollout 5G which will underpin the smart city initiatives across the country, as well as the proliferation of edge computing data centers and adoption of IoT devices.

However, the country is facing delays similar to the ones it faced with the launch of 2G, 3G and 4G, which only became available in India four to ten years after their global release.

A parliamentary panel on information technology headed by Congress MP Shashi Tharoor has recently alerted that 5G rollouts in India are most likely not going to begin until early 2022. Furthermore, India has still to go through its 5G spectrum auction which will last at least six months and is not expected to conclude in 2021.

Nevertheless, giant Jio announced last December that it intends to launch India’s first 5G network before the end of this year. Jio’s chairman, Mukesh Ambani has also said he intends to build 5G on indigenous hardware and technology components.

Other big names working to bring 5G to India include Airtel and Vi (Vodafone-Idea). Nokia, Ericsson and other telecom gear manufacturers are also working to help India enter the 5G age. Airtel has recently successfully trialed a 5G network in Hyderabad.

India’s Department of Telecommunications (DoT) has also taken the positive step to simplify and update laws – some more than 100 years old – that govern telecom services. This will enable 5G to be enjoyed to its fullest, permitting communication between devices, key to IoT and machine-to-machine (M2M) interaction.

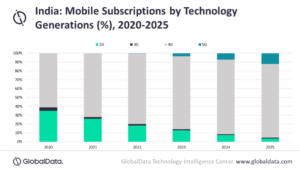

Whilst 5G is not available, 4G has become the prevalent network in India. Mobile subscription penetration in India is in fact set to cross 100% mark in 2023 from 88.3% in 2020, driven by growing smartphone adoption and increasing coverage of 4G- long-term evolution (LTE) services across remote areas, according to GlobalData.

Deepa Dhingra, telecom analyst at GlobalData, says: “4G will remain the leading mobile technology in India over 2020-2025 as operators such as Vodafone Idea and Airtel continue to expand their LTE networks. Moreover, operators like Airtel have been planning to completely reform the 3G network for 4G usage to drive 4G subscriptions.”

In a separate report, Ericsson shows to be optimistic about India’s 5G rollout and forecasts that 5G will represent around 27% of mobile subscriptions in India at the end of 2026, estimated at about 350 million subscriptions.

The Swedish multinational also estimates that by 2026, India will have 1.2 billion smartphone subscriptions, 390 million more than at the present. Mobile data in GB traffic per smartphone per month is also forecasted to more than double from 2020’s 15.7 to 37 by 2026.

IoT, Smart Cities and the Edge

Yet, nothing screams “Digital India” more than the IoT, smart cities and usage of edge computing. As previously mentioned, the $28 billion smart city rollout is one of Prime Minister Modi’s main flagship projects to modernize India.

The “Smart City Mission Transformation” is targeting 100 cities in four phases to drive economic growth and improve the quality of life of people by enabling local area development and harnessing technology, especially technology that leads to Smart outcomes such as smart lighting, smart bike sharing, asset tracking, to name but a few.

This will see wide adoption of IoT, from sensors to actuators, artificial intelligence software, machine learning and a wide range of other components that will modernize the nation’s infrastructure and people’s life.

Consulting firm Zinnov estimates that the IoT investments in India were close to $5 billion in 2019 and are expected to triple and touch $15 billion in 2021 across both technology products and services components.

The think tank highlights that by the end of 2019, India had 200-250 million connected devices. Zinnov estimates this number will grow tenfold to reach two billion devices by 2021, “signaling the exponential market growth in the next few years.”

Prankur Sharma, head of IoT practice at Zinnov, explains that India is one of the “most vibrant IoT ecosystems in the world.”

“The five major enablers propelling the Indian IoT market include the IT talent, the dynamic start-up ecosystem, the 10,000+ strong base of IT Service Providers, the robust digital infrastructure that the government is investing in, and the dedicated IoT Centers of Excellences (COEs) being set up,” he adds.

This explosion in the deployment and adoption of IoT devices across not just big metropolises but also Tier 2 and 3 cities – allied to the coming of 5G – is one of the driving forces behind the surge of Edge Computing developments that is only set to intensify in the coming years. Afterall, the IoT depends almost exclusively on accessing cloud networks.

The AdaniConneX JV will also focus on the deployment of smaller edge sites in addition to its larger data centers.

The edge sites will be strategically located throughout India and will support the need for more proximate capacity. These Edge sites will be designed and planned to easily scale with demand and become full scale data center campuses. Like the full-scale data centers projected in the JV, this pan-Indian platform of hyperlocal data centers will largely be powered by renewable energy.

All in All

It seems clear that India is on a journey to modernize its digital infrastructure and to build greenfield solutions as needed to serve underrepresented geographies across its territory.

With expansions set to transform urban centers’ connectivity and cloud capabilities, a key sub-trend worth keeping an eye out for is the development of data center campuses outside of India’s big cities. After all, “only” around 500 million people live in urban areas, compared to nearly 900 million in rural areas, according to MacroTrends.

With their AdaniConneX joint venture, EdgeConneX and Adani are poised to move quickly in a vast, underserved market, helping to bring services such as Cloud and Internet access to millions of Indian businesses and users.

As this massive, powerful nation develops its mass-scale smart city projects and migrates its government, enterprises and technology infrastructure to Cloud-based solutions, AdaniConneX will certainly help deliver a more digital future across the world’s largest democracy.

Check out the full video interview with Randy Brouckman, CEO for EdgeConneX and Jeyakumar Janakaraj, CEO for AdaniConneX HERE.