The shift in investment focus from purely the top four destinations – FLAP – is without a doubt a fascinating natural development and evolution of the industry in what is often considered a complex market for foreign operators. A blog by João Marques Lima.

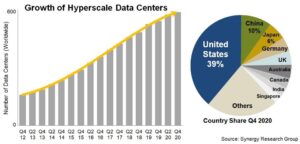

It wasn’t long ago that Synergy Research’s famous 600 hyperscale data centre sites figure made headlines all over the world. From the US to China, with Europe strongly represented in the middle, these “mothership” data center buildings are very much the core of the internet and our online – and some would say even offline – life.

In a separate report released in January, Technavio forecasts the global hyperscale data center market to grow by US$107.60 billion accelerating at a CAGR of nearly 27% during 2021-2025.

In a separate report released in January, Technavio forecasts the global hyperscale data center market to grow by US$107.60 billion accelerating at a CAGR of nearly 27% during 2021-2025.

Although the information technology industry is expected to witness mixed growth as a result of COVID-19, the impact of the pandemic on the market in focus is expected to remain positive, analysts say.

Just think of all the heavy-demand sparked by the pandemic – from working from home to more remote cloud gaming and CDN goods consumption. The list is huge.

Additionally, there has been for several years now a steady increase in demand for public cloud services, a rise in as-a-service based offerings, the construction of infrastructure for 5G and IoT technologies, and the use of advanced technologies, such as artificial intelligence, machine learning, deep learning and big data. All this drives hyperscale demand up.

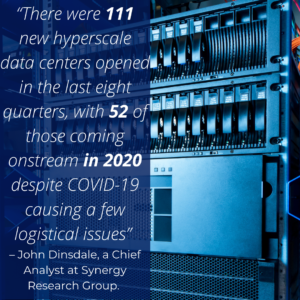

“There were 111 new hyperscale data centers opened in the last eight quarters, with 52 of those coming onstream in 2020 despite COVID-19 causing a few logistical issues,” said John Dinsdale, a Chief Analyst at Synergy Research Group.

“That is testament to the ongoing robust growth in the digital services that are driving those investments – particularly cloud computing, SaaS, e-commerce, gaming and video services. We did actually see a handful of older hyperscale data centers shut down in 2020, but those numbers pale besides the number of newly opened or planned sites.

“In addition to almost 600 operational data centers, we have visibility of a further 219 that are at various stages of planning or building, which is good news indeed for data center hardware vendors and wholesale data center operators.”

However, even though the rapid development of hyperscale sites is a global trend, in Europe, the movement is taking some remarkably interesting turns.

The continent’s data center markets that were once mostly confined to the big metropoles of Frankfurt, London, Amsterdam and Paris – the famous FLAP – are now witnessing the rise of other locations.

As I am writing this blog, the Ministry of the Interior in Luxembourg has, for example, just approved the partial development plan for a hyperscale data center facility by Google in Bissen, a town with roughly 3,000 people that sits at the geographical heart of Europe.

Hyperscale procurement of data center capacity in Europe is on the up and not going for the usual “location suspects” as colocation operators and big internet players like Facebook, Google, Apple, Microsoft and Alibaba continue to surf on a tide of digital demand that will not recede any time soon – and any time soon means many years to come, if it will ever recede.

Ireland, the Netherlands, Sweden, Finland, Italy, Switzerland, Spain – which we have recently covered – Wales, and Poland are some of the fastest growing locations of large-scale data center development in the Old Continent.

The hyper economy

Hyperscale investment does not come cheap, and the numbers are huge. For example, Google has of 2021 invested more than $14 billion in data centers and related infrastructure across Europe. This has in turn supported a further $18 billion of economic activity across, amounting to around 13,100 jobs per year on average, Copenhagen Economics estimates.

Similar figures can be found with Facebook, Microsoft and AWS, which have both over the years announced several $1, 2, 3 billion plus projects across the continent, mainly in Ireland and Northern Europe.

Large colocation players such as Equinix, Digital Realty, CyrusOne and Vantage Data Centers are all also devoting large sums of money to the construction of hyperscale sites as an answer to rising cloud demand.

Locally, Western Europe and the Nordic regions’ hyperscale data center market is forecasted to be generating revenues of around $29 billion by 2023, growing at a CAGR of approximately 10% during 2017-2023, says think tank Arizton.

The expanding hyperscale data center market also benefits a circular economy that has developed over the years to support hyperscalers. For example, the rapid expansion of hyperscale footprints in Europe is a major boost to contractors and sub-contractors operating in the market.

Power, one of the pillars of the data center world, is also benefiting from the development of hyperscale projects. Hyperscalers have historically been trendsetters and have also been at the forefront of many technological developments.

To that extent, they have been big on sustainability – and although much work is still needed – operators of large data center facilities are pushing through with their green agendas, which is in turn influencing more climate positive strategies from local grid operators and even boutique data centers.

An often barely spoken about benefit for telecom operators is the growing number of partnerships hyperscalers have established in Europe, leading telecoms to evolve into a new economic form that serves the digital world.

Hyperscale data centers are “connectivity-hungry”, therefore fiber, points-of-presence (PoPs) and internet exchanges (IX) are all benefiting from the boom in hyperscale development. This was the case of the MAREA subsea cable project, built through a collaboration between Microsoft, Facebook and Spanish telco Telefónica.

The development and decentralization of hyperscale sites from the FLAP regions is a trend that is not so much about what is to come, but what is being done in the field today. Across Europe, parcels of land are being primed for data center development, and a large chunk is being targeted at hyperscale players.

Digital demand will always win over complications and that demand is now forcing the data center to move to secondary markets that, as recently as one or two years ago, would not even be considered by many.

We’re in for a hyper-ride for sure!