By João Marques Lima

It is no secret that the data center market is booming across Europe, not only in the big cities of London, Dublin and Amsterdam, but also smaller markets such as Lisbon which in April saw as much as 650MW in data center projects announced.

However, whilst big facilities continue to be built across the continent, businesses have not forgotten the need for the edge. And how could they with COVID-19 pushing the need for computing literally to that edge?

First things first, edge computing is the idea of moving a good chunk of the data processes you would usually do in the cloud – primary data center – closer to the source of the data. This could be a server, an IoT device, even someone’s computer. You just got to be closer to the “edge”, to the data creation point to reduce latency and improve comms efficiency.

The most common example is driverless cars. The need for speed has never been so real and important with these vehicles. One millisecond could be the defining moment between life and death. A car driving at 130km/h on a German motorway does not have the luxury of time to send data back to a main city hundreds of kilometers away and wait for the data processing to happen and come back to it.

The analysis and action decision by the machine needs to be done locally. And whilst for long we talked locally in the sense of the car communicating to things such as lamp posts along the motorway, it will be more critical that the car does it all internally. Yet, it will still connect to the “grid” and yes, communicate with those lamp posts and more localized data center facilities, which will then be connected to the larger sites we all know. This is a new age for how we engineer the data center geographic network.

Whilst cars are just one example, across Europe much is being done in the digital and engineering space that is driving this demand for more data processing power at the source. More than 250 cities are being smartened up, hospitals are becoming tech hubs, schools are using a lot more digital platforms, street furniture is more intelligent than ever, transport systems are becoming automated and driverless, warehouses are taking in robots, businesses are taking more and more digital payments, streaming and gaming platforms are thriving, you name it.

On top of this, we cannot forget the impact that COVID-19 has had in shifting our routines from the office and a lifestyle of “out and about” to a more home-only scenario or majorly within a residential area for a long period. This has driven digital adoption and consumption across all the examples above at a more local level – from city centers and financial hubs to residential and farther away locations. We have covered some of this in a previous blog, where we looked at a McKinsey & Company report which has found that digital customer interactions have accelerated the equivalent of three years in the last one alone, whilst the share of products and services partly or fully digitalized have advanced the equivalent of seven years.

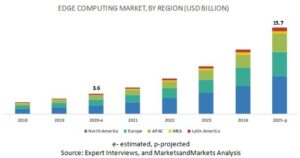

As a result of this growing demand for edge provisioning, the European edge computing market is expected to reach a value of US$1.94 billion by 2023, expanding at a CAGR of 29.3%, according to Kenneth Research and Research And Markets.

“Europe is progressing toward digital industrialization. Around 91% of European corporates are investing for the digitization of factory plants in the core of Europe,” analysts from the research houses say.

“Based on end-users industries edge computing networks are used in the manufacturing sector, energy and utility sector, IT and telecommunication, healthcare and life sciences, and consumer appliances. The IT and telecommunication sectors are expected to grab the largest market share. The region is leading in 5G deployment. The telecom operators in this region along with the US are expected to spend $185 billion by 2026 and the region is expected to have 214 million 5G connections by 2025.”

Some of the major Europe-based players in the edge computing space include Nokia (Finland), SixSq (Switzerland), German Edge Cloud (Germany), Saguna Networks (Israel), Altran (France), Ori (UK), Kontron (Germany), and EdgeInfra (Netherlands) to name but a few.

Big inter-continental players are also playing a fundamental role in the setting up of Europe’s edge play and speeding up investments, deployments, and available capacity. This includes for example,

Cisco (US), HPE (US), Huawei (China), IBM (US), Dell Technologies (US), AWS (US), FogHorn Systems (US), Vapor IO (US), GE Digital (US), Juniper Networks (US), and EdgeConneX (US).

Cisco (US), HPE (US), Huawei (China), IBM (US), Dell Technologies (US), AWS (US), FogHorn Systems (US), Vapor IO (US), GE Digital (US), Juniper Networks (US), and EdgeConneX (US).

EdgeConneX has in fact been a super active player in this space, having recently extended its presence to Barcelona, a tier 2 market that is proof of Europe’s edge bludgeoning landscape.

Whilst it comes as no surprise that Europe is rapidly building out its digital infrastructure and adoption of software that enables a more “edgy” world, it still is worth highlighting just how fast it is happening across the continent.

No longer are headlines solely focused on the larger metros, digital is giving the secondary and (soon we will see) tertiary markets, too, grabbing deserved attention.

Edge is giving us local democratization of digital access across borders and for Europe, this is not a matter of if or when, but of how fast we can go from this point forward.