João Marques Lima, JSA’s European Media Consultant, takes a close look at whether Europe can benefit from independent TowerCos.

Do you remember as a child riding in the car with your family through miles and miles of countryside? Counting those tall, strong masts that spread up until you could not see any more of them; counting the number of bird nests – especially stork nests; following the cables with your eyes up to the next tower?

Most likely, at the time you would not know that what you were looking at was part of a network of hundreds of thousands, millions of said infrastructures that connected the world. Those infrastructures last until today just like those memories.

![]() These towers continue to be erected across continents and are a key pillar of the digital infrastructure puzzle enabling connectivity and carrying data. From the tubular steel tower to reinforced concrete structures adorning the skyline, they give us the basis to build one big, connected world.

These towers continue to be erected across continents and are a key pillar of the digital infrastructure puzzle enabling connectivity and carrying data. From the tubular steel tower to reinforced concrete structures adorning the skyline, they give us the basis to build one big, connected world.

However, the tower landscape in itself is changing. For example, often when we talk about digital infrastructure, we do not think that even these constructions have had to spin their physical footprints to become digital themselves.

Digitalisation of towers and wireless infrastructure is just one of the trends currently transforming the sector in Europe. Going green or a large wave of asset consolidation are also other movements in this space.

Towers provide an important element for the operations of wireless network services, including mobile networks, fixed wireless access broadband, emergency services, TV and radio broadcast, internet of things (IoT), and private mobile radio (PMR) networks. The largest user segment of towers are the mobile network operators (MNOs).

In the report, “The economic contribution of the European tower sector”, Ernst & Young LLP’s (EY) Olivier Wolf (partner, EY and EMEIA TMT leader for EY-Parthenon) and Ulrich Loewer (associate partner at EY and TMT telecoms strategy also for EY-Parthenon) highlight that over the last couple of decades, tower ownership has increasingly been transferred from MNOs to separate tower companies (TowerCos).

“These TowerCos can take the form of an internal division within an MNO, a separate entity controlled by an MNO or a wholly independent entity,” Wolf and Loewer explain.

The original TowerCos business model blueprint was first conceived in the US in the mid-’90s as an alternative to captive MNO tower ownership. Since then, the tower industry has become both more diverse and mature. Today, TowerCo business models differ by region but generally fall under three broad categories, including joint venture TowerCos, MNO-controlled TowerCos and independent TowerCos.

According to Alex Mestre, Business Deputy CEO, of tower giant Cellnex, industry participants are recognising the value independent TowerCos deliver.

“This includes the economic value, which is widely described,” he says in the EY report. “There are further elements, though — this relates to the ecological landscape, as people can benefit from the coverage without too much impact on the environment. We also have the financial capacity to deploy infrastructure as fast as policy makers and the population expect. Lastly, we have deep industrial knowledge and technical expertise.”

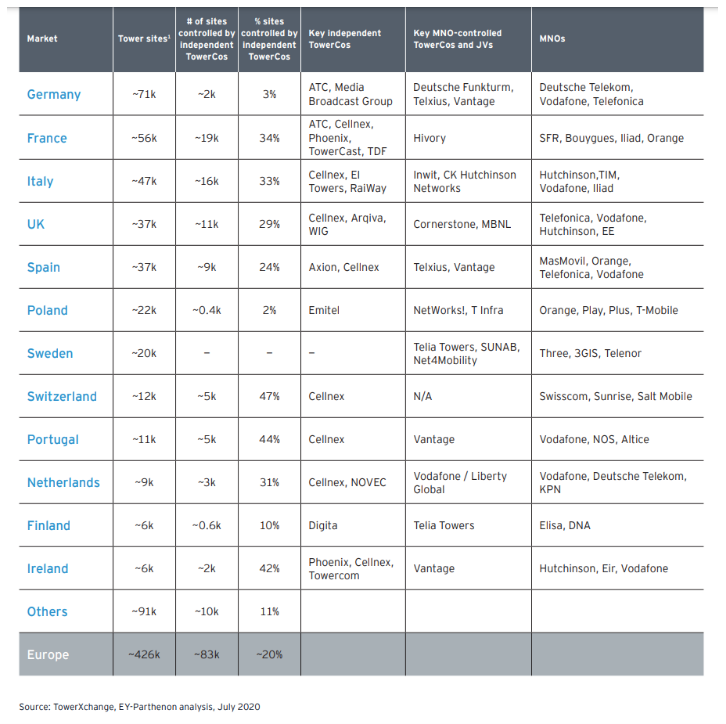

The latest stats point to 426,000 tower sites in Europe today, including rooftops and other larger structures that are used for wireless communication (but excluding small cells and DAS). Morgan Stanley estimates that by 2025, this number will top 450,000.

As much as 60% of the market is concentrated in Spain, the UK, Italy, France and Germany, with the latter being the country with the largest number of towers in Europe at more than 71,000.

Tower growth is estimated at approximately 1%–3% annually for the next five years, especially driven by 5G deployments.

Wolf and Loewer point out that the past few years have seen the share of towers directly owned by MNOs decline, while the share of towers controlled by independent TowerCos has grown significantly from 13% (in 2014) to 20% in 2020, with an acceleration in the last two years.

A lot of this change has been driven by MNOs carving out their tower portfolios in separate MNO-controlled TowerCos. Transactional examples include, for example, TIM carving out Inwit in Italy, Altice carving out SFR TowerCo in France.

Further consolidation of MNOs has helped with this trend, such as the acquisition of E-Plus by Telefonica in Germany.

The joint venture set up by Bouygues/SFR in France paints the picture on a new wave of JVs set up by MNOs to pool passive infrastructure resources.

Additionally, tower portfolio divestments from MNOs to reduce debt and raise cash for investment in core business activities, while independent TowerCos actively pursue in-organic growth strategies, has been another driver for the increase of independent TowerCos.

Lastly, EY points out that independent TowerCos are growing organically and/or building towers in build-to-suit programs for MNOs, such as Cellnex building towers for Bouygues in France.

However, it is important to highlight that despite the growth in independent TowerCo ownership in Europe, the continent is still fairly lagging most other regions. For example, the share of towers held by independent TowerCos in the US at the end of 2020, was 90%, the highest percentage of any region.

This is followed by Central and Latin America at 55%, India at 52% and Sub-Saharan Africa at 42%. Only South and South East Asia stay behind Europe, but by a difference of just 1%.

Scott Coates, CEO, Wireless Infrastructure Group, says: “Europe still trails other global telecoms markets when it comes to the penetration of independent infrastructure operators. This is changing rapidly as our more efficient business model for many types of infrastructure unlocks increased investment and better connectivity.”

TowerCos Success

In terms of benefits, independent TowerCos play an important role in enabling the telecoms industry to make most efficient use of its passive infrastructure. The higher utilisation rates of independent TowerCos reduce the cost per user, lowering the threshold at which it becomes profitable to improve service coverage.

EY’s Wolf and Loewer point out five main benefits including:

- A more efficient market structure;

- By selling towers to independent TowerCos, MNOs retain capital to further invest in existing and new services within their portfolio;

- A stronger footprint for more investment in capacity and coverage;

- Easing of market-entry barriers to non-MNO tenants;

- And a more sustainable approach to infrastructure management.

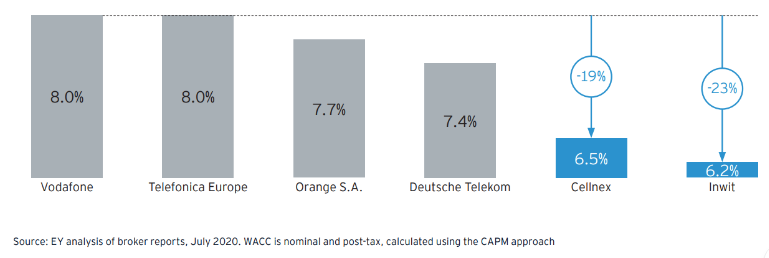

Overall, EY estimates that greater tower outsourcing could result in an economic saving in Europe of €31 billion (or US$36.76 billion) between 2019 to 2029.

“Our analysis assumes a 3% annual net growth in points of presence over the next 10 years,” Wolf and Loewer say.

![]() They further add that since 2018, the share of independent TowerCos in Europe has increased from 17% to 20%, helping to release c.€3.5 billion of capital in the process via acquisition of tower portfolios from MNOs. An additional €28b of capital could be released if the rate of outsourcing in Europe grew to 50% in the future.

They further add that since 2018, the share of independent TowerCos in Europe has increased from 17% to 20%, helping to release c.€3.5 billion of capital in the process via acquisition of tower portfolios from MNOs. An additional €28b of capital could be released if the rate of outsourcing in Europe grew to 50% in the future.

“We consider an outsourcing rate of 50% to be an upper estimate of the level of outsourcing possible in Europe, recognising that existing joint ventures between MNOs limit the level of outsourcing to an extent,” it reads in the report.

“Recent transactions provide support for this — since 2018, as their share of sites grew from 17% to 20%, Independent TowerCos have helped release circa €3.5 billion in capital via acquisition of various tower portfolios from MNOs. In addition, significant amounts are invested by independent TowerCos in Build to Suit programs, thereby helping MNOs avoid the corresponding capital.”

The Future of TowerCos in Europe

The question in the end is if TowerCos will become the predominant business model for tower operations in Europe. The answer is likely to take a few years to shape itself up, but the benefits are there: TowerCos deliver cost-saving, faster-market deployment, and a more climate friendly approach to the tower business.

Historically, Europe has lagged behind on such transformational trends, with the US leading the charge and driving in the investment and influence for change. Will things follow suit here? Only time will tell.