A feature article by JSA European media consultant, João Marques Lima.

Germany is the second largest data centre colocation market in Europe, with an estimated revenue of over US$1.2 billion generated in 2021. And Frankfurt accounts for a large portion. Here’s why.

Being Germany’s business and finance capital, Frankfurt has built a name for itself in the data centre world and is today one of the leading global destinations for capital deployment in the sector.

With a strong power supply and network routes, the German city’s hosting firms deal with customers mainly in the financial and banking services, commerce, and manufacturing industry – Germany being a global industrial powerhouse.

The data centre economy here is so important to the local GDP, that in 2020, German power grids and utility firms spent over US$900 million to meet data centre power demands in Frankfurt.

Frankfurt has ranked as one of the most desirable locations for some years now – and not only among the FLAP markets. In Germany especially, Frankfurt with its expanse is by far the most important market for data centres in the field of colocation and cloud.

“The significance of Frankfurt as a data centre site is also evidenced by the presence of a large number of data centre operators in the local market such as Interxion, Equinix, Digital Realty, Telehouse, e-shelter, and Global Switch, to name a few,” explain CBRE’s Michael Dada (director of data centre solutions), Tobias Jermis (senior director of valuation advisory services), and Dr Jan Linsin (managing director and head of research) in their “Data Center Market: Germany” report.

At the same time, Frankfurt is the world’s largest Internet exchange point. The volume of data transmitted via the DE-CIX Internet exchange point with its fibre optic cables meanwhile averages more than six terabits per second. During the Covid-19 pandemic, this reached as high as ten terabits in November 2020.

The size of the Frankfurt market is set to have reached a growth rate of more than 408.47% by the end of 2021, from 118MW in 2010 to over 600MW by 31 December 2021, CBRE estimates.

The size of the Frankfurt market is set to have reached a growth rate of more than 408.47% by the end of 2021, from 118MW in 2010 to over 600MW by 31 December 2021, CBRE estimates.

“More data centres are currently in the pipeline. Consequently, the offering of computing capacity is set to increase in the future,” researchers say based on several expansion announcements. “The offering of data centre capacity in Frankfurt is being developed in line with increased demand.”

However, in its latest quarterly report covering Q3 uptake and supply, CBRE adverts that the data centre industry is waiting to hear what restrictions, like energy conservation measures, if any, the Frankfurt Government will impose on its development efforts.

“Potential government-imposed restrictions on build activity remain an overhang for operators in Frankfurt. Supply constraints and higher costs for colocation operators are issues as well,” says Andrew Jay, head of data centre solutions.

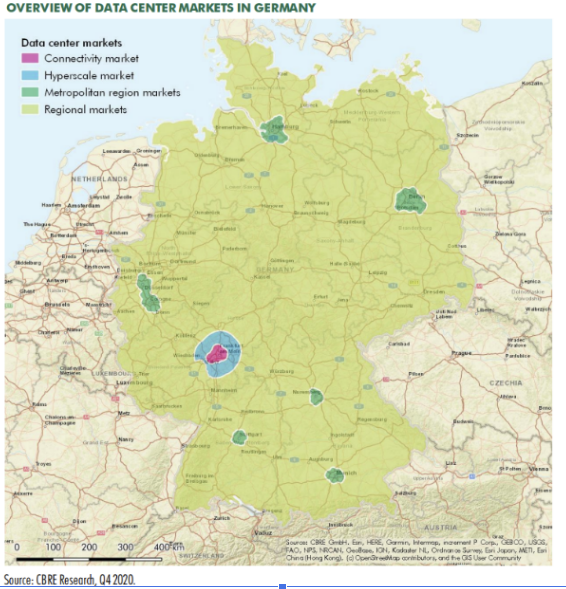

But Frankfurtk’s data centre monopoly does not restrain itself with the city’s official 248.31 sq Km/95.87 sq mi of land. While colocation data centres initially clustered around Internet exchange points, the requests for hyperscale data centres requiring plenty of space have extended the market territory into the greater Frankfurt region.

“As the choice of a site is generally contingent on very good data connection as many different transmission operators as possible, colocation and hyperscale data centres will stay concentrated in Frankfurt and in the metropolitan regions for the foreseeable future,” CBRE says. “Edge data centre operators specialised in providing data centre capacities in direct customer proximity may develop blanket market coverage.”

Who’s expanding?

Simply said: everyone. Frankfurt’s data centre market main investors include today players such as China Mobile International (CMI), Colt Data Centre Services, CyrusOne, Datacenter One, Digital Realty, envia TEL, Equinix, Iron Mountain IO, KeyWeb, Maincubes One, NDC-GARBE Data Centers, NewTelco, NTT Global Data Centers, Penta Infra, Vantage Data Centers, and noris network.

Being a manufacturing and industrial economy, Germany has attracted several data centre construction contractors and sub-contractors, which are also aiding in building out Frankfurt’s footprint. Some of the key names here include AECOM, Arup, Collen Construction, DPR Construction, ICT Facilities, KLEINUNDARCHITEKTEN, Lupp Group, Max Bogl, Mercury Engineering, M+W Group (Exyte), Royal HaskoningDHV, STS Group, Winthrop Engineering, and Zech Group.

Supporting the digital infrastructure economy are also several other household names of the likes of ABB, Caterpillar, Cummins, Delta Electronics, Eaton, KOHLER-SDMO, Legrand, Rolls-Royce Power Systems, Piller Power Systems, Riello UPS, Rittal, Schneider Electric, Socomec, STULZ, and Vertiv.

Some of the recent projects that have grabbed headlines for their magnitude, include CyrusOne’s planned 90MW expansion in Frankfurt with the construction of a fifth building in the city. The earliest phase of construction is planned for Q2 2023 with the first phase of 9MW of capacity or more delivered Q3 2024.

Some of the recent projects that have grabbed headlines for their magnitude, include CyrusOne’s planned 90MW expansion in Frankfurt with the construction of a fifth building in the city. The earliest phase of construction is planned for Q2 2023 with the first phase of 9MW of capacity or more delivered Q3 2024.

Matt Pullen, EVP and managing director Europe, CyrusOne, said: “Take-up in capacity by hyperscalers continues to drive significant demand for data centre needs across Europe, resulting in near record levels of construction pipeline, particularly in Frankfurt.

“CyrusOne has enjoyed remarkable success in the region and a fifth site in Frankfurt signals our experience in this market and our capability to consistently deliver mission-critical capacity and capabilities that our customers have come to depend on.”

Another example of expansion comes from central European data centre operator maincubes which has also recently unveiled plans to “invest hundreds of millions of euros” in a second colocation facility in Schwalbach, near Frankfurt. With operations at the FRA02 data centre scheduled to commence in summer 2023, the new facility will include 75,350 sq ft/7,000 sqm of white space for IT plus office space, and have a power capacity of 20 MW to serve a non-disclosed “major tenant” that has already been signed.

Yet, questions are expected to arise in the coming months and years as to markets like Frankfurt will be able to sustain their record year after record year growth rates, especially taking into account the potential new government-led restrictions on the sector.

To that extent, Tash Mehta, Associate Director at VIPA Digital, says: “While the mature markets of Frankfurt, London, Amsterdam, Paris and Dublin continue to grow at pace, a high cost of entry and locational constraints such as access to power and network capacity can erode the returns when compared to emerging EMEA locations.”